Investing In Annuities– Tax Benefits & Drawbacks

Last week, we talked about some basic features of investing in annuities. We highlighted how variable annuities come with potential drawbacks, and yet many people still choose to buy them. What gives?

Part of the reason is probably misinformation and irrational fear of stocks.

If you aren’t knowledgeable about investing in annuities and you are scared of losing money in stocks, a good sales guy could probably sell you any type of annuity based on the “safety” sales pitch — but remember that the sales guy gets a commission if he convinces you to buy the product.

In reality though, the money you put into a variable annuity will likely be partially invested into the stock market anyway.

This is not to say that variable annuities are necessarily bad. The point is that even if the salesperson says they are “safe,” they still have market risk.

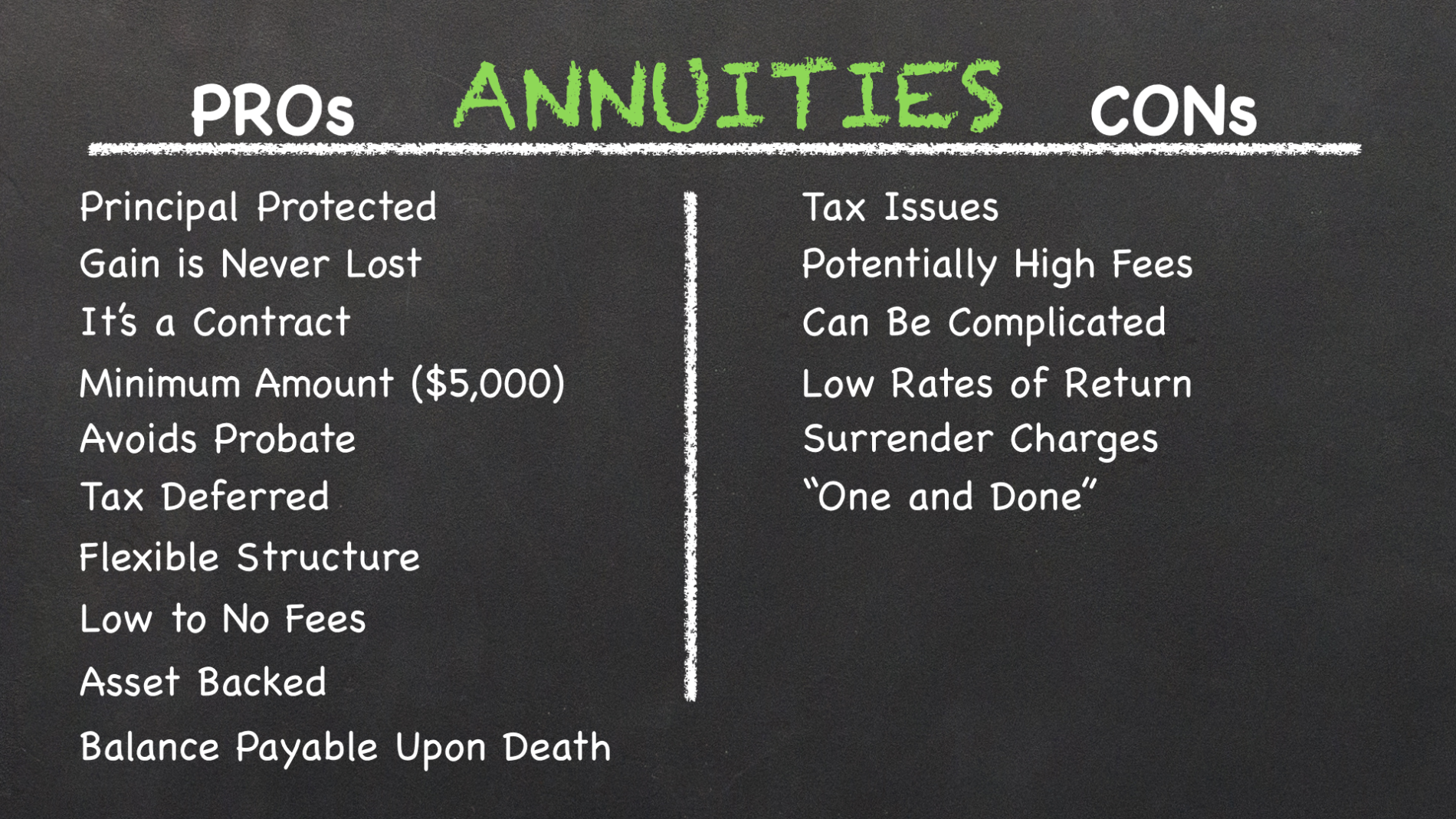

Variable annuities do allow your investment to grow tax deferred until you start to receive distributions from the annuity. If you bought the annuity with after-tax dollars, the IRS will tax you only on the portion exceeding your original contribution.

However, if you bought the annuity with pre-tax dollars, such as money in a traditional IRA, the full distribution would be taxable. When you contribute to a traditional IRA, your taxable income is reduced by the amount of the contribution, up to the allowed maximum amount, but investing in an annuity does not reduce your taxable income.

In any case, a fixed annuity would have given you the same tax deferment benefit, with lower fees. A key drawback with a fixed annuity, though, is that it’s vulnerable to inflation risk.

When Do You Want to Get Paid?

The other major issue to consider when investing in annuities is how and when you want to start to receive cash back.

If you want to receive money very soon after you buy the annuity, you will want to choose an immediate annuity. In this case, you will begin to receive payment usually within 60 days of signing the contract and funding the annuity.

The other choice is a deferred annuity. You will have to wait for a specified period of time before payment begins. The time between purchase of an annuity and the start of payments is the accumulation phase, where the money you invested in the annuity, ideally, grows. Most annuity contracts will guarantee that, in the event the annuity investor passes away during the accumulation period, the beneficiary or beneficiaries will receive either the premium paid or the accumulated value of the contract, whichever is greater. So it’s very important to name a beneficiary and read the terms of the agreement.

Important Choices

You can also choose how you want your distributions. You can receive one lump sum distribution from the annuity or receive scheduled installments. If you choose the second option, there are additional choices to make.

You can choose the life-only option. The insurance company will send you regular payments for as long as you live. However, if you happen to pass away soon after the annuity starts paying out, this would turn out to be a very bad deal. The annuity payments will end, and the insurance company keeps whatever remains.

The second option is life with a certain period. Under this arrangement, you still get paid for as long as you live, but there’s also a guarantee that it will pay for a specified number of years. For example, if the annuity is life with 10 years certain, and you pass away in year 7, your beneficiary would still get 3 additional years of payments.

Another choice is joint life with the last survivor. In this case the annuity covers the primary owner and a beneficiary, usually the spouse. The insurance company will continue to make payments until both spouses die.

Essentially, think of it as a life-only annuity, but for two people. A significant downside to this option is that upon the death of one spouse, the payments to the surviving spouse will be smaller than the combined payment may be to the couple when the first spouse was alive.

Given the risk of dying prematurely and losing everything invested into the annuity, you may wonder why anyone would choose the life-only annuity.

Larger Potential Payments, Greater Risk

One reason is that the investor may not be aware that there are other choices. Another reason is that the scheduled payment installment under this plan is usually greater than the other two choices mentioned here. Consequently, if you live for a long time after the annuity begins to pay out, you will end up receiving the most money back under this plan.

No one shoe fits everyone. Whether annuities are right for you really depends on your investment goals and other factors such as risk tolerance. If you decide to invest in an annuity, I stress again the importance of carefully reading the contract and watching out for unreasonable fees or conditions.

Sharing is Caring. Feel free to share this article with a friend or fellow investor.