Investment Adviser

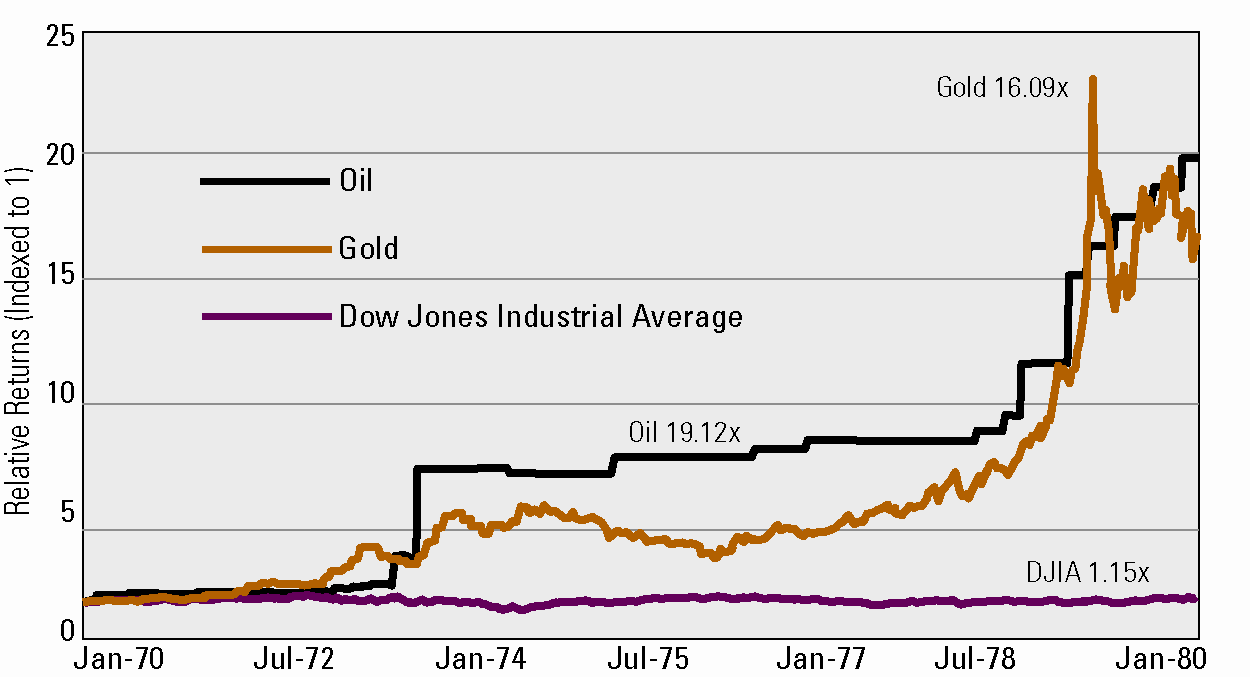

History Lesson: Select Hard Assets vs. Stocks in the 1970s

Investment Strategy Communicated With Transparency

Dr. Stephen Leeb serves as the President, Research Chairman, and Chief Compliance Officer of Leeb Capital Management, an SEC-registered investment advisory firm. He has authored nine books on various economic and investment topics. In addition, he serves as the Editor of Turbulent Time Investor (“TTI”), an online newsletter focused on investing. TTI is published by TCI Enterprises, LLC, a separate company also owned by Dr. Leeb. The recommendations in the newsletter are general investment opinions and recommendations, not individual investment advice and should not be construed as personalized investment advice.

This activity is separate and distinct from the investment advisory services of LCM. LCM does not manage client portfolios based on the strategies or recommendations included in the newsletters. LCM’s clients can, however, acquire securities that are recommended in a publication. LCM, at all times, strives to act in the best interest of clients and to treat all clients in a fair and equitable manner. When trading securities of companies that are discussed/recommended in the newsletters to which LCM employees contribute content, in keeping with its fiduciary duty owed to advisory clients, LCM will transact in the securities prior to the release of the newsletters. Noting that the investment parameters of newsletter subscribers may differ from those of LCM’s clients, it is possible that LCM may act on behalf of LCM’s clients in a manner contrary to the recommendations provided in the newsletter subscribers.

Nothing on this website should be constructed as a solicitation or offer, or recommendation to acquire or dispose of any investment or to engage in any other transaction. LCM does not render or offer to render personal investment advice or financial planning advice through our website.

Viewing or utilizing information on this website, or contacting or responding to our offices or investment adviser representatives does not create an investment advisory relationship of any kind. An investment advisory relationship can only be established and investment advice can only be provided after the following three events have been completed: (1) LCM’s thorough review with you of all the relevant facts pertaining to a potential engagement; (2) the execution of a written LCM engagement and fee agreement; and (3) delivery of the LCM Form ADV disclosure brochure.

For more information, please see our ADV.